Preparing for 2025

2025 is poised to be a transformative year for the life sciences industry, marked by significant innovation and heightened competition. As life sciences companies prepare for launches in the year ahead, it will be crucial to navigate evolving regulatory environments, shifting patient needs, and rapid technological advancements.

Key considerations for a successful 2025 launch include prioritizing access / value-based healthcare, leveraging digital technologies, and navigating a dynamic M&A environment. By understanding the trends shaping the industry and current launch best practices, companies large and small can position themselves and their assets for success. A patient-centric approach, coupled with a strong emphasis on data-driven decision-making, will be essential to drive innovation and deliver life-saving therapies to patients in 2025.

2024 Recap

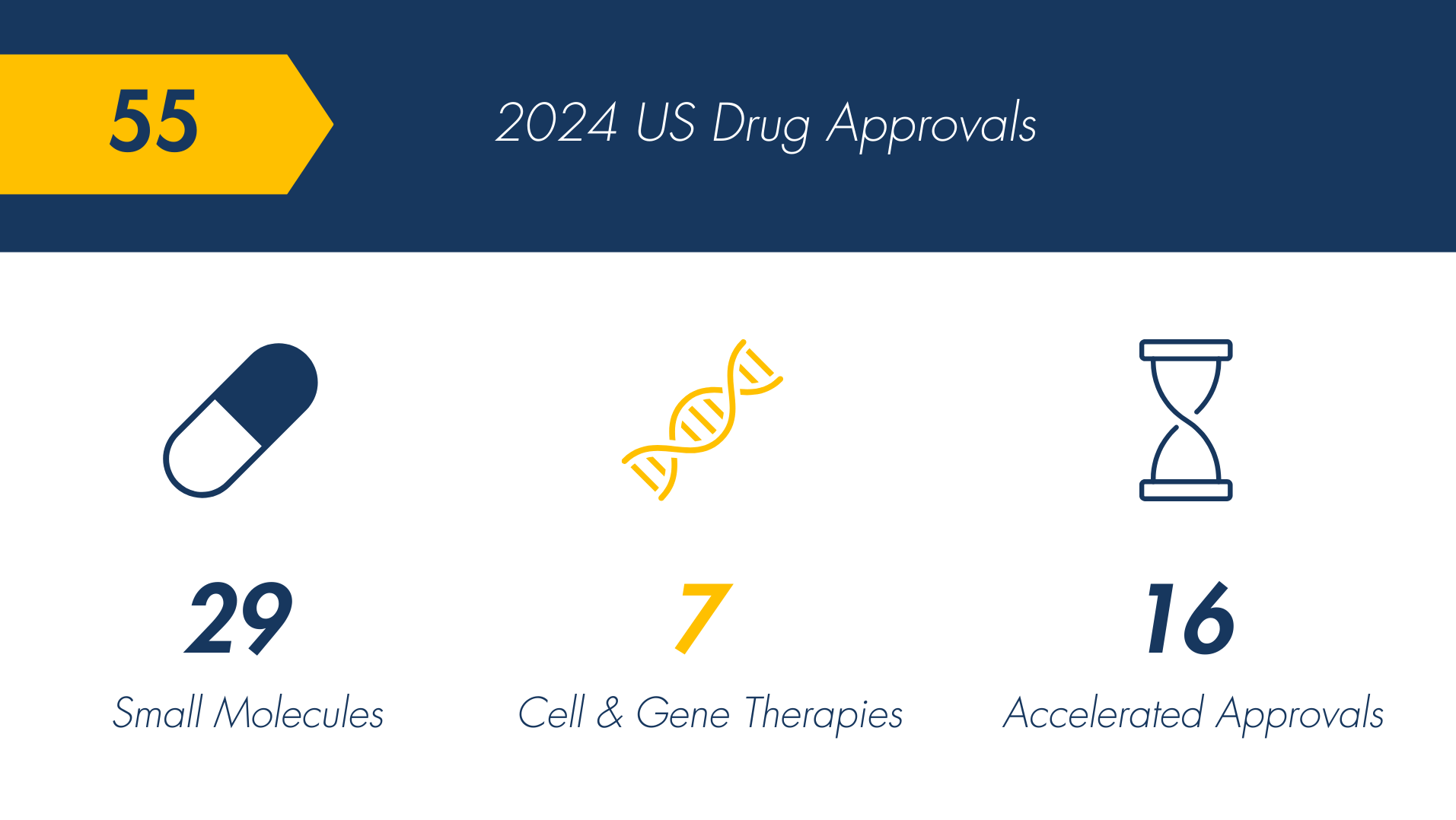

Last year, the US saw 55 novel drug approvals (47 via CDER, 8 via CBER), a decline from 66 approvals in 2023.¹

Of those approved:

- The relatively high number of small molecule approvals indicates continued industry focus on this therapeutic class.

- Cell & gene therapies have reached an all-time high. This trajectory is expected to persist, alongside the associated costliness. Last year, Lenmeld ($4.25M) became the most expensive drug in 2024, far surpassing the price of Hemgenix ($3.5M).

- Accelerated approvals (among novel drugs) reflect the FDA’s focus on approving treatments with ongoing Phase 3 trials that can address significant unmet needs.2,3

We expect that several medications approved last year will significantly impact treatment paradigms in their respective spaces for years to come: COBENFY in schizophrenia, Kisunla in Alzheimer’s, and Yorvipath in hypoparathyroidism. As we enter 2025, many of us will be closely monitoring uptake and working to accelerate the adoption of these innovative therapies.

Marketplace Trends in 2025:

1. Therapeutic Areas of Focus

2025 is shaping up to be a year of continued investment, with a particular focus on oncology (~19 assets), metabolic & inflammation (~6 assets), and CNS therapeutic areas.4

- Oncology: As many as 14 tumor types stand to see new treatment approvals in 2025, oncology continues to command significant investment and attention. In non-small cell lung cancer (NSCLC) and breast cancers, industry watchers are particularly focused on the groundbreaking bispecific antibody ivonescimab (Summit Therapeutics), innovative drugs like Dato-DXd (AstraZeneca) and inavolisib (Genentech), alongside label expansions for recently approved treatments like Enhertu (Daiichi Sankyo/ AstraZeneca). Merck and Bristol Myers Squibb are investing billions of dollars into developing innovative immunotherapies and targeted therapies. This area saw record-breaking M&A deals in 2024, and the trend is expected to continue as companies seek to expand their pipelines and market reach.

- Metabolic & Inflammation: With rapid growth driven by the likes of Novo Nordisk’s Wegovy and Ozempic, the obesity drug space is expected to reach an eye-popping $105B in 2030, up from an earlier Morgan Stanley forecast of $77 billion5, Roche’s Carmot Therapeutics acquisition underscores GLP-1 & metabolic disorders innovation. In the year ahead, we expect to see a number of innovative treatments and line extensions targeting a wide range of disease states [e.g., Non-Alcoholic Fatty Liver Disease (NAFLD), Polycystic Ovary Syndrome (PCOS), and neurological disorders].

- CNS: Companies like Biogen and Alzheon are making significant investments to pursue novel approaches to treating Alzheimer’s disease and other neurodegenerative disorders. Cobenfy’s full-scale commercialization (BMS) is expected to transform schizophrenia treatment, providing the first new mechanism of action in a decade.

2. Competitive Pressures and Market Access Evolution

- Pricing and Market Access Challenge: The role of formulary decision makers (e.g., payers, employers, governments) in treatment decision-making has only intensified as our systems manage the delicate balance between innovation and affordability. To be commercially successful, manufacturers need an increasingly sophisticated understanding of pricing, reimbursement, and formulary inclusion dynamics. In spaces with innovative treatments and high costs (e.g., obesity, Alzheimer’s, Cell & Gene Therapies, Rare Diseases), this balance will continue to limit uptake and increase pressure on evidence-generation programs.

- Payer / PBM Concentration: The increasing concentration and consolidation of payers and PBMs has only led to increased pricing pressure, an increased administrative burden, and restricted market access for manufacturers, ultimately impacting profitability and the availability of new medications to patients. Any delays in access can significantly reduce a drug’s overall revenue potential, and poor access strategies can produce suboptimal patient outcomes and erode trust in the healthcare system more broadly.

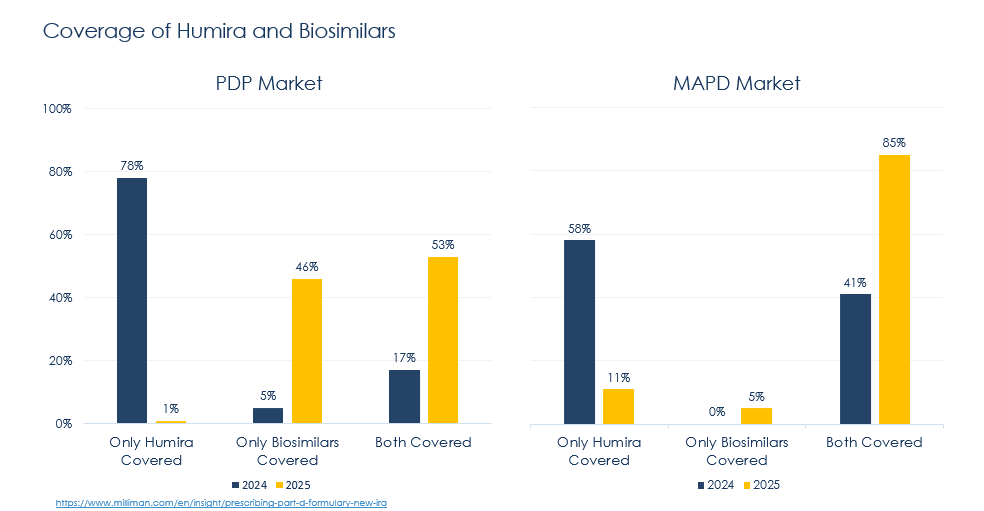

- Generics and biosimilars: The influx of generic and biosimilar competition has hastened the erosion of patent exclusivity, further eroding revenue streams. All told, biosimilars have commanded ~53% market share 5 years post-launch (with higher uptake in Oncology – e.g., Bevacizumab, Trastuzumab) and slower uptake in immunology. At the same time, average sale price (ASP) has declined by the same number, 53% on average, 5 years after the first biosimilar launch (even more aggressively in mature markets)6. AbbVie’s Humira continues to face headwinds from biosimilars in the year ahead: following CVS Caremark’s lead, additional PBMs are planning to exclude or otherwise restrict Humira in 20257. Much of the shift occurring this year can be attributed to changes in the IRA’s Part D redesign.

8

3. Favorable M&A Environment

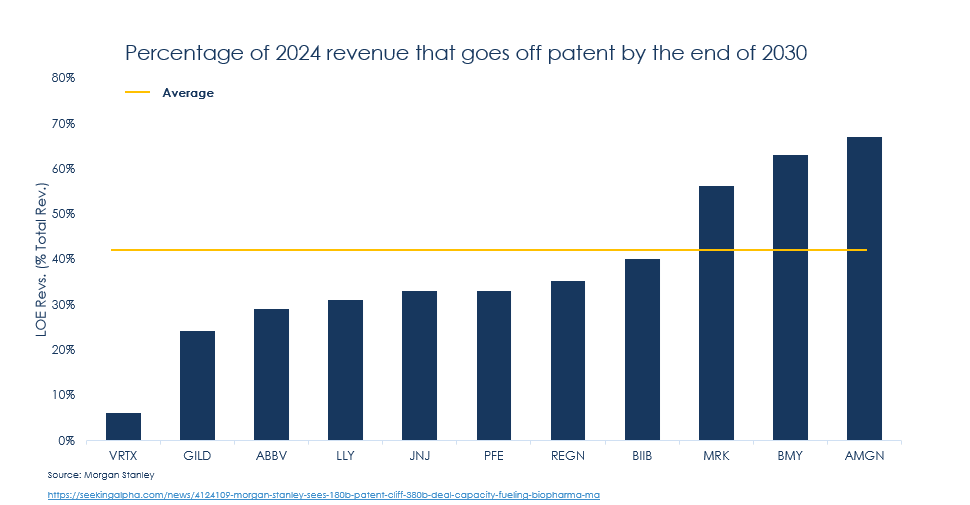

- Patent Cliff: After relatively muted M&A activity in recent years, 2025 is poised for increased activity, driven by the need to offset an estimated $183.5 billion in annual sales at risk due to patent expirations by 2030.9

- Dry Powder among Big Pharma: Morgan Stanley analysis indicates that experienced manufacturers such as J&J and Novo Nordisk will leverage significant financial resources (~$383.1B), to acquire new later-stage assets and sustain growth10. Merck is particularly well positioned due to its balance sheet strength to offset the LOE risk for its blockbuster: Keytruda. Recent deals of note include:

- BMS: Acquired Karuna Therapeutics to offset 64% of projected 2025 revenue at patent-loss risk (driven by Eliquis)

- Amgen: Acquired Horizon Therapeutics to offset 42% of projected 2025 revenue at patent-loss risk (Prolia, Enbrel, Xgeva, and Repatha)

- Deregulation: Many expect that a shift in leadership at the DOJ and FTC will enable larger mergers due to a more favorable regulatory environment in the US, addressing concerns that have stalled such deals in recent years.

10

- Launch Implications: manufacturers should continue to monitor late-stage assets changing hands, particularly to experienced manufacturers with established commercial engines, and scenario plan based on a shift in the competitive dynamic.

4. Oversight & Policy Uncertainty

- Dynamic Political Climate: The current political environment is introducing potential changes in drug pricing, approval rates, and regulatory oversight that could significantly impact the pharmaceutical industry and healthcare stakeholders.

- Anticipated Policy Adjustments: Industry stakeholders are closely monitoring potential shifts in FDA leadership and regulatory policies, which could influence drug approvals, pricing strategies, and market dynamics.

- The Future of IRA & Legislative Priorities: While President Trump has de-emphasized his previous support for reducing drug prices in his current campaign, significant interest remains in the Senate and House to repeal the IRA’s drug price negotiation program; industry lobbyists are pushing to delay small-molecule drug price negotiation eligibility by four years, positioning this as a bargaining tool for broader legislative priorities.

- Emerging Leadership Impacts: Key appointments, such as individuals with critical views on pharmaceutical practices, could reshape the regulatory landscape, influencing approval timelines and pricing frameworks.

Commercial Launch & Marketing Implications in 2025

1. Digital Transformation and Data-Driven Commercialization

- Leveraging Digital Channels: The rise of digital marketing and personalized medicine plays a crucial role in 2025. Pharmaceutical companies can leverage social media, SEO, and interactive content to engage patients and healthcare professionals. Successful campaigns have shown improved awareness and uptake of new drugs through tailored and targeted messaging.

- Data Analytics for Optimized Decision-Making: Data analytics empowers manufacturers to make informed decisions. For instance, companies that analyze patient data can fine-tune their targeting and resource allocation for launches. This leads to more effective marketing efforts and reduced waste in spending. Click here to read a case study of a targeted patient population analysis.

- Building a Robust Omnichannel Strategy and Ecosystem: Creating a seamless patient journey requires an integrated approach to marketing. Combining digital and traditional channels enhances patient engagement. Best practices include using email campaigns alongside social media outreach to ensure consistent messaging.

2. Ensuring Market Access through Value-Based Healthcare and Alternative Channels

- Value-Based Pricing and Reimbursement Models: The shift toward value-based healthcare impacts how drugs are priced. In 2025, more companies will explore pricing models linked to patient outcomes. While challenges exist in the current negotiation process, and very few value-based contracts are in currently in place for specialty drugs (a recent survey suggests <10% of health plan managers are utilizing11 ), improved data systems and changing incentives within the health system will continue to be driving forces. Click here to read a case study of a successful value-based contracting strategy.

- Real-World Evidence Generation: Real-world evidence (RWE) is becoming increasingly important in 2025. Companies can use RWE to demonstrate their products’ effectiveness in everyday settings. For example, biopharma firms that employed RWE in their marketing campaigns observed improved acceptance rates from healthcare providers. Click here to read a case study of a successful evidence-generation strategy for a first-in-class therapy launch.

- Specialized Care Models: The high costs associated with specialty drugs necessitate innovative care models to enhance patient retention and lifetime value. Strategies include patient support programs & digital health initiatives to fully maximize the product’s revenue potential. Learn more about the impact of support programs on therapies for complex conditions.

3. Patient-Centric Strategies & Execution

- Defining Patient Needs: While market research has long been utilized to gather insights on patient preferences, patients are increasingly taking an active role in their own treatment and, as a result, manufacturers are developing and implementing targeted launch plans that address the specific needs of different patient subpopulations.

- Patient Support Programs and Adherence Initiatives: Effective patient support programs can enhance treatment adherence. By addressing barriers like medication complexity, companies can improve patient outcomes. Companies are increasingly incorporating digital health tools into launch plans to enhance patient engagement and support adherence. Click here to read a case study on transforming the patient access journey for a rare disease asset.

- Direct-to-Consumer (DTC) and Alternative Models: Eli Lilly and Pfizer both launched platforms this year that allow patients to buy medications and other health products without visiting a doctor or pharmacy in person (LillyDirect and PfizerForAll). Driven by improvements in technology and consumer buying behaviors, innovative manufacturers are increasingly exploring similar programs, and alternatives, to simplify the patient experience and provide patients to access medications they need.

4. Next Level Launch Excellence – Beyond “Project Management”

- In dynamic and rapidly changing markets, it is increasingly important to leverage proven models and specialized expertise in pharmaceutical product launches to develop adaptive, patient-centered strategies that address unmet needs and proactively identify and mitigate risks to ensure launch success.

- Pharma launch offices are adopting digital tools, agile methods, and patient-focused strategies to enhance efficiency, collaboration, and outcomes.

- Digital tools and platforms are being increasingly utilized to enable real-time tracking, collaboration, and communication; at the same time, virtual and remote launch activities help teams reach a wider team and reduce costs.

- Experimentation with agile methodologies and other operating models to quickly adapt to changing market conditions and increasingly cross-functional launches.

- Teams have increased emphasis on scenario planning and are implementing more robust risk management processes to identify and mitigate potential barriers to success. Click here to read a case study of a successful mock launch workshop for entering a new disease state.

Herspiegel leverages proven models and our collective knowledge, to develop tailored, patient-centered strategies that ensure alignment across teams, mitigate risks, and drive consistent, predictable success. We have helped life sciences companies launch more than 125 innovative therapies into even the most complex markets. Herspiegel is here to help to accelerate time-to-market and optimizing launch outcomes.

Meet the Experts

References

¹ https://www.fiercepharma.com/pharma/2024-drug-approvals Note: this summation includes approvals for biologic therapeutics and vaccines but excludes diagnostic imaging agents, which are represented on the FDA’s full list.

² https://www.fda.gov/media/151146/download?attachment

4 https://www.norstella.com/practice-changing-drugs-2025/

6 SAMSUNG BIOEPIS Biosimilar Market Dynamics 7th Edition, Q4 2024

8 https://www.milliman.com/en/insight/prescribing-part-d-formulary-new-ira

11 https://link.psgconsults.com/2024-trends-in-specialty-drug-benefits-report